Credit risk refers to the risk of loss a lender faces when borrowers fail to repay their loans. It is a critical factor in the lending industry, impacting the decisions of banks, credit unions, and other financial institutions.

Why Credit Risk Matters

- Financial Stability: High credit risk can lead to significant financial losses for lenders.

- Interest Rate Determination: Lenders use credit risk to set interest rates; higher risk usually translates to higher rates.

- Regulatory Compliance: Financial institutions must manage credit risk effectively to comply with regulatory standards.

- Portfolio Health: Managing credit risk is essential for maintaining a healthy and profitable loan portfolio.

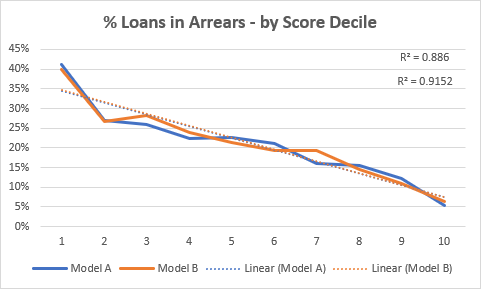

Traditional Measurement of Credit Risk

Credit risk assessment traditionally relies on:

- Credit Scores: The most common method, utilizing credit scores from credit bureaus.

- Credit History: Reviewing borrowers’ past credit behaviors, including payment history and credit utilization.

- Debt-to-Income Ratio: Evaluating the borrower’s existing debts relative to their income.

- Collateral Value: Assessing the value of collateral, if any, offered against the loan.

Alternative Data in Credit Risk Assessment

Alternative data has become increasingly valuable, especially for assessing “thin-file” borrowers who are new to credit or have limited credit history.

- Mobile Phone Data: The mobile network, line type and tenure of a mobile phone number provides insights into a customer’s previous repayment behaviour and affordability.

- Email Address: The history of an email address, including age and reputation provide insights into both credit and fraud risk.

- Utility and Rent Payments: Regular payments for utilities or rent can indicate financial responsibility.

- Bank Account Analysis: Insights into cash flow patterns, savings, and spending habits.

- Educational and Employment History: Stability and potential earning power can be gauged from educational and career backgrounds.

- Social Media Data: Some lenders analyze social media behavior, although this is more controversial and raises privacy concerns.

Importance of Alternative Data

- Wider Inclusion: Helps in evaluating those without extensive credit histories.

- Behavioral Insights: Provides a deeper understanding of a borrower’s financial behavior.

- Risk Diversification: Enables lenders to diversify their portfolio by confidently lending to a broader demographic.

- Competitive Advantage: Lenders using alternative data can cater to underserved markets, gaining a competitive edge.

Conclusion

Credit risk is a pivotal aspect of the lending process, directly influencing the profitability and sustainability of financial institutions and loan providers. While traditional credit risk assessment methods remain foundational, the integration of alternative data is revolutionizing the field, particularly in assessing the creditworthiness of those with thin or no credit history. This shift not only expands the market for lenders but also opens up opportunities for a wider range of borrowers to access credit.

How can Honey Badger help?

Honey Badger is a leading provider or alternative data for credit risk analysis. Integration with mobile network operators allows us to provide real-time data that supports decisioning, especially for thin file or new to credit customers. To find out more visit Honey Badger’s Risk Insights page.