What is KYC?

Know Your Customer (KYC) is a critical process used predominantly in the banking and financial sector to verify the identity of customers. This procedure involves assessing the risks associated with a business relationship, crucial for preventing illegal activities such as identity theft, financial fraud, money laundering, and terrorist financing.

Purpose and Users of KYC

The main goal of KYC is to ensure legal compliance, manage risks, and prevent financial crimes. It’s not just limited to banks and financial institutions; insurance companies, investment firms, real estate businesses, and fintech companies, particularly those dealing with digital payments and cryptocurrencies, also implement KYC practices.

How KYC Works

KYC involves the collection and verification of customer information, including:

- Identity Verification: Verifying the customer’s name, date of birth, and address through official documents like passports, driver’s licenses, or utility bills.

- Due Diligence: Conducting background checks to assess the customer’s risk, including checking against watchlists and sanction lists.

- Ongoing Monitoring: Regularly updating customer information and monitoring transactions for suspicious activities.

Types of KYC

KYC can be divided mainly into traditional and electronic KYC (e-KYC). Traditional KYC involves in-person verification and manual checks, whereas e-KYC leverages digital methods and biometric technologies for efficiency and speed.

KYC in Fraud Detection

Implementing KYC is pivotal in fraud detection and prevention. By verifying identities, tracking financial transactions, and enhancing the security of these transactions, KYC plays a vital role in reducing unauthorized or illegal financial activities.

The Challenge of Friction in KYC

While KYC is essential, it can create friction in customer experience, leading to challenges like:

- Longer Onboarding Times: Extensive checks can delay account opening or service access.

- Invasive Processes: Customers may be uncomfortable sharing personal information.

- Technical Challenges: Difficulties with online verification methods or document submissions.

- Customer Dropouts: Frustration with the process can lead customers to abandon the service.

Light vs Heavy KYC

The concept of ‘light’ and ‘heavy’ KYC addresses this friction. Light KYC involves basic identity checks and is usually the first step, ideal for low-risk services or as a way to quickly eliminate bad actors before proceeding to more detailed KYC checks. It is quicker and less intrusive. On the other hand, heavy KYC is more comprehensive and includes in-depth background checks, typically reserved for high-value transactions or services with higher risk profiles.

Tailoring KYC to Individual Needs

Recognizing that KYC isn’t a one-size-fits-all solution is key. A tiered approach is often more effective, starting with light KYC for most customers and escalating to heavier checks for high-risk scenarios or when suspicious activities are detected. This approach helps in balancing the need for security and legal compliance with maintaining a positive customer experience.

KYC remains an indispensable tool in the financial and business world, striking a balance between security, legal compliance, and customer experience. By understanding and appropriately applying light and heavy KYC measures, organizations can both safeguard against fraud and cater to the varying needs and risk profiles of their customers.

How can Honey Badger help?

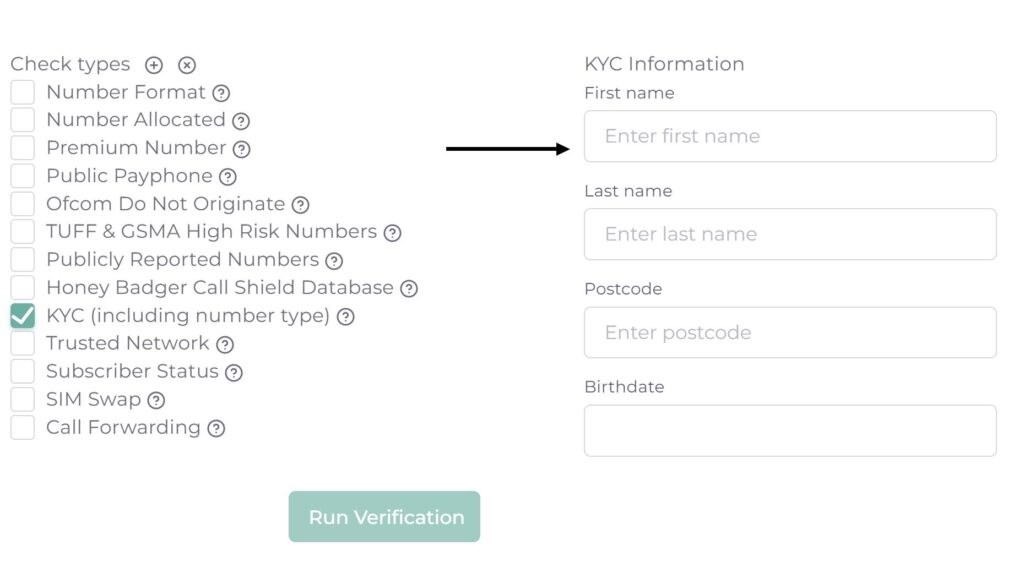

Honey Badger is a leading provider of light KYC checks that can happen instantly and without any customer friction. For example, personal information can be verified against the data held on file my mobile network operators. This provides a lost cost way of ensuring the customer information matches a trusted and verified third-party data source. To find out more visit Honey Badger’s Risk Insights page.