It’s not if, but rather when, will regulation descend on the world of Buy Now Pay Later (BNPL) like a dense fog on the high seas? When it does arrive, regulation will focus on ensuring adequate affordability and credit checks take place, which immediately brings the ‘F’ word to mind – friction that is.

But while some BNPL providers will undoubtedly run aground navigating the journey ahead, others will adapt, survive, and prosper. How? By utilizing alternative data sources in new and novel ways, BNPL providers can comply with regulation without adding friction – and unlock opportunities to reduce fraud while increasing their addressable market. Let’s take a deeper look…

First things first, consider how BNPL has largely operated up until now. Think instant approval with little or no interest payments. The upside being that merchants can increase sales by offering consumers flexible payment options but without carrying the risk of nonpayment. While BNPL providers benefit from this by taking a percentage of all sales they facilitate, it’s not without risk and some serious potential downsides.

The need for (1) frictionless and instant decisions compounded with (2) pressures from merchants who require minimum approval rates severely limit the extent that risk checks can be performed. The result is significantly higher rates of fraud when compared to traditional (regulated) lending approaches. Furthermore, credit risk is also greatly increased since affordability checks are limited by time and friction constraints. Either way, borrowers that never intended to repay or those that just can’t afford to repay are bad news for BNPL.

These risks are somewhat more exaggerated with BNPL versus traditional lending approaches given consumer demographics. Studies have shown that consumers aged 18-24 are the most reliant on BNPL services. This means a significant portion of BNPL consumers are ‘new to credit’, thus little or no data is available in credit bureaus to backup lending decisions.

The Risk with Regulation

So far, proposed regulation in the UK has focused on bringing protections commonly seen with loans and other forms of credit to BNPL. For example, requiring affordability checks prior to approval that ensure payment plans are affordable for consumers. While these protections are undoubtedly beneficial in safeguarding consumers from taking on unmanageable levels of debt, they pose the following threats to BNPL providers:

Adding additional checks increases friction for consumers in terms of both time and effort. This leads to higher abandonment rates causing merchants to lose sales.

More stringent affordability checks lower approval rates, which has a significant impact on merchants who lose potential customers.

For new to credit consumers little or no data exists to carry out checks, further reducing the approval rate and making BNPL less attractive to merchants.

It remains to be seen whether BNPL protections will be an extension of existing regulation, or if entirely new regulation will be introduced that better meets the somewhat unique way that BNPL services work. Either way, BNPL providers can expect the future to hold requirements for more rigorous checks that are intended to show lending decisions are made with demonstratable evidence of affordability.

The BIG opportunity for BNPL

The success of a BNPL service is inherently linked to its ability to provide high approval rates while minimizing the amount lost to fraud and nonpayment. Many have speculated that the introduction of regulation will primarily put downward pressure on approval rates, therefore challenging the long-term feasibility of BNPL. However, this hypothesis is usually based on the assumption that BNPL services will need to leverage the same high friction data sources traditional loan and credit providers use to determine affordability (I.e. credit bureaus and Open Banking data).

The real opportunity for BNPL is not with retrofitting existing methodologies, but instead leaning deeper into alternative data sources that comply with regulation whilst also increasing approval rates and reducing fraud. But what exactly are the alternative data sources that BNPL services can leverage?

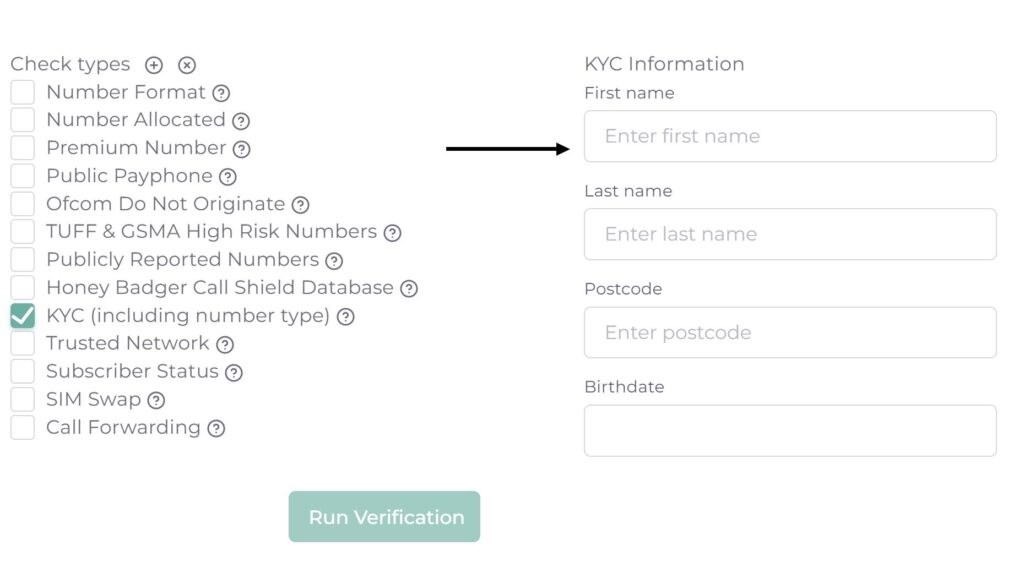

In recent months Honey Badger has worked with lenders to evaluate how predictive mobile intelligence data is. This is data that can be extracted or determined from a consumer’s mobile phone number and typically includes the following:

Mobile network provider

Line type (pay-as-you-go vs pay monthly)

KYC verification on first name, last name, date of birth and/or postcode

Whether the device is overseas

Whether call forwarding is setup

Whether there has been a recent SIM Swap

This information can be determined instantly and without any friction for the consumer, which is a key requirement for BNPL providers. But most importantly analysis shows a clear and predictable correlation between these data points and the likelihood of fraud or nonpayment. In essence, consumers on top-tier networks, on a pay-monthly contract and with fully verified identity details (determined by comparing against the data held on file by mobile network operators) are significantly less likely to default on their repayments. So much so that for the lenders we worked with, propensity to go into arrears could be determined with an almost identical level of accuracy as Open Banking.

The opportunity for BNPL services to capitalize on mobile intelligence data doesn’t stop there. Globally, 98% of Gen Z owns a smartphone. In contrast, it’s estimated that 29% of Gen Z don’t have a credit score, or at least don’t know if they have one. This is significant given that it’s Gen Z consumers that rely most on BNPL.

Finally, for BNPL services to thrive there must also be a meaningful reduction in fraud. Fraud signals, such as whether a mobile device is overseas, if call forwarding is enabled and if there’s been any recent SIM swaps are proven and effective ways to identify high risk consumers. Identity verification checks made against the data held by mobile networks further enhances this. The combination of KYC verification and mobile fraud signals provide BNPL providers with an opportunity to protect against multiple different types of fraud, including account takeover and synthetic identity theft.

Beyond Mobile Data

Don’t stop with mobile insights, alternative data sources can even include basic contact information, such as an email address.

Did you know that newer email addresses are significantly more likely to be fraudulent?

And that the reputation of an email address provides insights into malicious or high risk behavior.

While confirming social profiles are linked to the email address increases the likelihood you’re dearling with a genuine person.

In Summary

The future of BNPL isn’t as bleak as some may suggest, if BNLP providers can move quickly to incorporate alternative data sources like mobile phone intelligence, that is. Ultimately the future of BNPL will lie in its ability to embrace non-traditional data sources to comply with regulation, rather than applying existing methods which would corrode the very essence of what makes BNPL valuable to both merchants and consumers.

If you’re a BNPL provider with the impacts of complying with future regulation on your mind, drop us a message and we’ll show you the power of using alternative data sources like phone numbers, email addresses, IP addresses and location to increase approval rates and reduce fraud.

Speak with an expert

Enter your email address and we’ll arrange

Honey Badger HQ