Podcast alert! Honey Badger CEO Matthew Salisbury recently joined the wonderful Bradley Chalupski of Merchant Fraud Journal on the To Catch a Fraudster Podcast.

Podcast alert! Honey Badger CEO Matthew Salisbury recently joined the wonderful Bradley Chalupski of Merchant Fraud Journal on the To Catch a Fraudster Podcast.

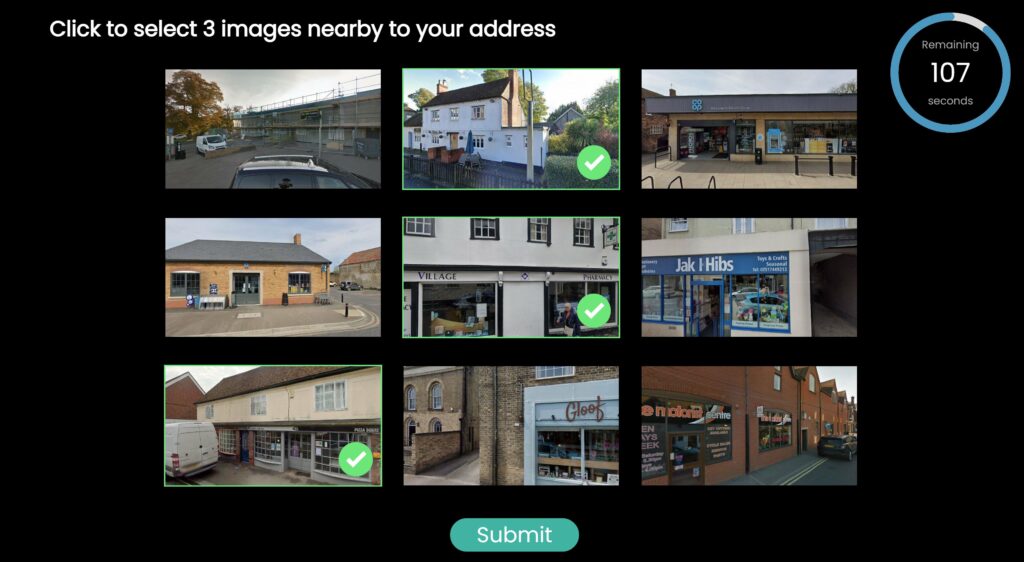

Matt and Bradley discussed everything – from how Honey Badger’s founding team first got started fighting fraud, to how Geo Authentication has emerged as an additional security layer. Listen now ⬇️